Advertisement

Understanding Tax Audits in Canada

CRA Audits Part 1 - The Process

by L. Kenway BComm CPB Retired

This is the year you get all your ducks in a row!

|

Sip your tea while we chat about self-employed tax audits work in Canada. |

U.S. AuditsLooking for information on American (U.S.) Audits by the IRS? This link will take you to the IRS publication "Examination of Returns, Appeal Rights, and Claims for Refund". The IRS video, "Your Guide to an IRS Audit" is also worth a peek at if you received an IRS audit notification. |

Advertisement

Tax Audits - Four Part Series

click on image below to go to chat

Chat 1

Tax Audits The Process |

Chat 2

Receiving a Tax Notice |

Chat 3

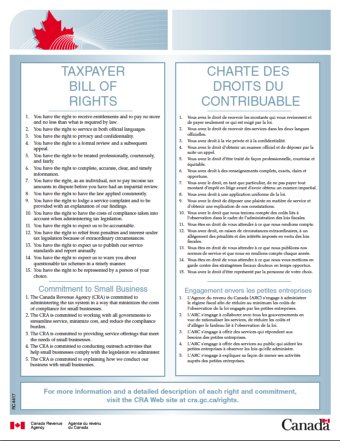

Taxpayer Rights |

Chat 4

Voluntary Disclosure |

You've refilled your tea or coffee cup? Let's start then .

What It Means When You Sign Your Income Tax Return

Once tax preparation is complete, your final step is to sign your income tax return. What does it mean when you put pen to paper? ... or hit the online send button?

You should know that when you sign your income tax return, or remit it electronically, you are stating that your return is correct and true. It is irrelevant who prepared your return - you, your spouse, a friend, a relative or a tax preparation professional.

When you sign the return you are accepting the burden that everything has been reported accurately and legally within the framework of tax law in Canada. There were two recent court cases (2015) where this was put to the test.

It is your responsibility to have knowledge of and apply the tax laws correctly. Having a professionally prepared income tax return by a competent tax preparer ensures a return will stand up to a CRA audit.

The Difference Between a CRA Review and CRA Audit

Canada's tax system depends on self-assessment by taxpayers. To determine compliance with Canadian tax law, the Canada Revenue Agency (CRA) conducts review activities. Generally, there is a high degree of public compliance with the law.

Good To Know

During reviews, CRA tries to educate you, the taxpayer, in addition to verifying your income reported.

If you receive a request for documentation or receipts under the review process, it does not mean you are being audited.

If you are being audited ... you will receive a notice explaining you have been selected for an audit ... and arrangements will be made for a meeting ... to begin the audit.

Tax Reviews - The Pre-Assessment Review

Once your return is filed, CRA does a pre-assessment review prior to issuing the Notice of Assessment. They do a quick check for arithmetic errors and check various deduction and credits on the return. No manual reviews are done at this point.

The peak period for doing this type of assessment is February to July. Once this review has been performed, a Notice of Assessment is issued. If you have a tax refund, it will be released at this time ... but be aware that if the more detailed reviews performed after the tax season determine there was an error, you may have to give some of that tax refund back ... so don't spend it too quickly.

The Notice of Assessment

The first document you will receive, usually about two to six weeks after you file your return, is your official Notice of Assessment. This is an important piece of paper. File it with your tax return. It has important information that will be required when you file next year's return.

If no problems have been found on the initial filing, the return will confirm your numbers.

If a problem was found, an explanation will be given and adjustments will be made by CRA to your return. You may have additional taxes, interest and penalties to pay.

You have whichever is the latest date of:

- one year from your tax filing due date, June 15 if you are self-employed; or

- 90 days after receiving the Notice of Assessment

to file a Notice of Objection if you disagree with the assessment. (If the numbers have been reassessed and you had a tax professional prepare your return, notify them immediately ... because sometimes CRA assessors do make mistakes.)

As a general rule, CRA can only change a return three years (statue of limitations) after the Notice of Assessment has been issued ... unless you are suspected of misrepresentation or fraud ... then there is no limit.

If numbers involve carry backs or investment tax credits, the limit is extended to six years.

Review this table of relevant tax compliance timelines. It is your responsibility to be aware of these time frames.

Tax Reviews - The Processing Review

After the tax season is over, between June and November, CRA conducts most of their processing reviews (which is similar to the pre-assessment reviews). It is a more thorough review of deductions and credits and may involve manual review.

Between September and March, the matching program is in full force.

This is when information filed is compared to third-party sources such as employers or financial institutions.

It's goal is to ensure the correct net income for tax purposes is reported ... as many of Canada's federal and provincial tax credits and benefits are dependent on this number.

It is important to note that if the CRA determines that a return under claims credits relating to CPP or at source tax deductions, an adjustment is made and if applicable, a refund is issued.

How Returns are Selected for a Tax Audit

In a Financial Post story on January 2, 2008 entitled Audits do not happen randomly, the commissioner and chief executive of CRA said during a talk to the Canadian Tax Foundation, that returns are selected for additional scrutiny because of a deduction claimed or an industry that is being focused on.

Based on the above three preliminary tax pre-audit reviews, your return may be selected for a more detailed tax audit. The selection process for individual returns may have a random selection process but are normally selected for the following reasons.

- for comparison to third party information

- missing information found under the matching program

- for certain types of deductions or credits claimed

- due to the individual's tax audit history ... you were audited previously and it resulted in an adjustment

Business returns are sorted and grouped by the CRA computer system ... then audit selection may be for one of the following reasons:

- random selection based on computer generated lists of audit projects testing a particular group of tax payers identified as having high non-compliance

- leads from information from other audits, investigations or informants

- association with other taxpayers who were selected for audit

No distinction is made based on the filing method nor on who prepared the return.

Office Audit (Tax Reviews) versus Field Audit (Tax Audits)

If you are selected for an audit, the tax auditor will perform an office audit or a field audit.

In an office audit, the auditor reviews your records at the CRA office. The majority of audits are office audits. You may not even meet with the auditor. Sending in the requested information to support your claim may be enough.

Office audits are part of the review process and CRA does not generally consider these true audits. They reserve that honor for the ... field audit.

During a field audit, the auditor comes to your place of business at a pre-arranged time. If you have an accountant representing you, the auditor will meet with your accountant at a pre-arranged time and place with the necessary support documents required.

Any unsupported claims will usually be denied. Storing your tax returns and supporting documents in one place each year will make a future audit proceed smoothly ... no running around trying to gather information ...

... soooo remember to put back any pieces of paper you remove from your bookkeeping box ... otherwise you undo all your audit proofing efforts. :O(

What Happens in Tax Audits?

The main purpose of the audit is to monitor and maintain the self-assessment system mentioned at the beginning of this discussion. An income tax audit used to be combined with a GST audit, but that practice stopped in 2010 when BC and Ontario introduced HST.

During a tax audit, your ledgers, journal, bank documents, source documents such as sales invoices and expense receipts will be examined to ensure they support your claim. Vehicle logs will be perused. Issues will be identified and discussed. You may be requested to tape list receipts.

An audit is not a cause for concern ... unless you have engaged in tax avoidance or tax evasion.

You can have someone represent you in an audit. You do not have to meet the tax assessor alone.

Proposals will be made during the tax audit by the assessor. Always ask for these proposals to be put in writing. You will have 30 days to respond. Consideration will be given to your responses before the Reassessment Notice is issued.

Here's what you should do if you receive a notice saying you are being audited.

The Notice of Re-Assessment

Once you receive your re-assessment notice, arrange to pay any additional tax, interest and penalty charges. If you disagree with the notice ... you have 90 days from the date of the notice to file a Notice of Objection.

The Knowledge Bureau have 2 excellent articles on the 2 choices available to you if you want to object. The January 25, 2012 article looks at the formal tax court procudure while the November 4, 2012 article looks at the pros and cons of the informal procedure which is less costly and less time consuming.

The January 25, 2012 article very briefly provides an overview of both procedures. Here is an excerpt:

"The Informal Procedure is available only if the total disputed tax amount (other than interest or provincial tax) does not exceed $12,000, the amount of loss in issue does not exceed $24,000, or the only amount disputed is interest ...

General Procedure is a formal litigation process that begins in the Tax Court of Canada and can proceed, if unresolved, through the Federal Court of Appeal right up to the Supreme Court of Canada. Going through this general court process is usually lengthy — there is no pre-determined time frame and can take several years — and very costly. It applies to disputes in which federal taxes exceed $12,000."

BOOKKEEPER'S HANDY REFERENCE

CRA Videocasts

Located midway on the right hand side of the page at cra-arc.gc.ca> Learn more/Get help> Videos> Videos and recorded webinars for businesses (previously it was Media> Videocasts> Videos for businesses) you will find a CRA videocast called What To Expect From An Audit which covers much of the same information discussed here.

The videocast is interspersed with question and answer periods recorded during the live seminar which are helpful in understanding the process.

Knowledge is understanding.

Hopefully this article has helped you understand the process of tax audits ... alerted you to your responsibilities with regards to filing your tax return ... and given you a better understanding of why it is so important to have accurate bookkeeping records that assist you in being audit-proof.

Audit proof books are your best defense.

It's been great chatting with you.

Your Tutor

Main Source of Information for this article: CRA publications found at Businesses > Changes to your business > Audit ... Individuals > Tax return > Review of your tax return by CRA ... IC 71-14R3t The Tax Audit