- Home

- Accounting System Setup

- Chart of Accounts

Your Chart of Accounts

The Blueprint of Your Small Business Accounting System

by L. Kenway BComm CPB Retired

This is the year you get all your ducks in a row!

Published January 2014 | Edited June 1, 2024

Your chart of accounts (COA) is the blueprint of your accounting system around which everything is built. If your COA is poorly designed, the quality of your information is affected ... which could affect the business decisions you make using the information.

What Is The Chart of Accounts? How Does It Work?

So if you haven't guessed, your COA is a list of all the accounts in your accounting system. You use it to categorize then record your transactions onto ledger pages ... each account listed in your COA has its own ledger page. If you use the computer, it is an electronic page.

All the ledger pages from all the accounts listed in the COA are called the general ledger (GL).

When you want a financial report, the accounts (ledger pages in the general ledger) are summarized to produce the financial report requested.

Normally the chart is numerical but with small business accounting systems like QuickBooks, it no longer has to be numerical due to auto recall. A list comes up as you type in your letters allowing you to select the account you want.

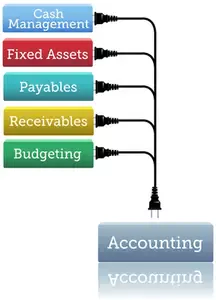

COA are usually organized into seven sections that are used to summarize transactions for your financial statements. Do you recognize these categories from your balance sheet and income statement?

The Bookkeeper's Tip

Leave Space Between Numbers

If you choose to have accounts numbers in your COA, don't make them sequential like 1001, 1002, 1003, etc.

Instead leave spaces for growth like this: 1000, 1010, 1020, etc.

- assets [1000 series]

- liabilities [2000 series]

- equity [3000 series]

- revenue [4000 series]

- cost of goods sold (COGS) and expenses

[5000 and 6000 series] - other revenue [7000 series]

- other expense [7000 series]

How To Use Your COA

Your chart of accounts is something you should print out and carry with you (like a shopping list) until you become familiar with it.

When you purchase something, write on the receipt what account it should be coded to by looking through your COA listing and selecting the appropriate account.

The Bookkeeper's Tip

Develop this routine NOW

... while things are simple.

Make this a rule ... Each time you make a purchase for your business, take an extra moment to jot down on the receipt the account number or expense category -- before you forget.

Your bookkeeper (which may be you ... or not!) will love you. Everything gets entered into the correct expense category. No more scratching your head wondering what in the heck you bought or why.

Don't know your account numbers or expense categories ... then you should carry your chart of accounts around with you like a shopping list until you do!

How To Setup Your Chart Of Accounts

The Bookkeeper's Tip

Parent Accounts vs.

Sub-Accounts

If you use QuickBooks, it is perfectly fine to code entries directly to an account with no sub-accounts.

If a "parent" account has sub-accounts, it is better to code directly to a sub-account.

Some advisors recommend never coding to the parent account if you have sub-accounts. Personally, I'd rather have you code to the parent account if none of the sub-accounts are quite right and you don't know where else to code. It's a quick fix for ProAdvisors so don't worry yourself over it.

- If your internal financial statements are prepared on a tax basis, a good place to start is to have your COA based on tax form T2125. You can tailor it to your specific business later if need be ... but it won't be necessary for most small businesses.

For my American visitors, take a look at the tax form Schedule C (form 1040) to get started. You can find a copy on the IRS website www.irs.gov. You will find a link to the form under Businesses> Small Business/Self-Employed> Self-Employed.

If you use QuickBooks, they have a whole selection of preset COAs. Just pick the one that is structured for your industry. Again, you can customize it later. QuickBooks has the ability to assign an account to a tax line ... so you don't have to organize your COA for tax purposes. You can organize your COA for your business or industry ... and let the tax mapping report assist you come tax time. It's the best of both worlds. - You never want to have accounts that are too specific.

For example, an account called utilities is good ... because it is generalized; an account named after a single customer or vendor such as Telus or BC Hydro is not so good ... because it is too specific. (see sidebar.) - There should be NO duplicate accounts. If there are, merge them into one account. If you have different departments or locations, a software program like QuickBooks can be setup to track them using classes, but it is NOT done through multiple accounts.

As a general rule, an account should NOT be named after one product or service such as Size 10 Pants or Short Haircuts. It is better to name the account Clothing or Haircuts.

This rule applies to the naming of sub-accounts too!

- Each account should be properly classified into one of the seven sections discussed above. This means capital asset accounts for equipment purchases should NOT be found in the expense account section.If

you are using QuickBooks software, make sure you have setup the correct

type of account ... not every account is a bank account type (the

default). Loan accounts should be setup as a long term liability type NOT an income type.

- A good COA shouldn't need more than 50 or so accounts in a small business. If you have too many accounts, you are likely to have a lot of accounts with small balances under $100. It just doesn't provide useful information at that level and creates a lot of maintenance as each account has to be reconciled regularly. Fewer accounts will ensure you have greater consistency in where transactions are coded and recorded. This means you are more likely to have accurate financial statements you can rely on.

The Bookkeeper's Tip

Where To Capture Your Online Advertising Fees?

Create one sales account called Affiliate / Advertising Income. Record all these types of income there ... no sub-accounts required.

Sales from eBooks or webinars should go to one account called Website Sales or eProduct Sales. You get the idea.

You do NOT create sub-accounts to track the income from various customers or products.

For example, if you earn Google Adsense income or affiliate fees / commissions on your website, do NOT make sub-accounts called Google Adsense, AWeber, etc.

If you want to know how much income you have earned from Google Adsense or any of your affiliates, run a Customer Sales Summary or Detail report.

Better yet, learn how to create a customized report to track your top ten customers.

Learn the best way to record your affiliate and advertsing income payments in QuickBooks here.

See you on the next page ...

Your tutor

You might like these

How To Send Sensitive Information Online

Sending sensitive information in an email is NOT a good idea. Explore your options on how to best transmit financial documents online to prevent identity theft.

Evaluate Your Book Keeping System

Whether you are just starting out or have been in business awhile, how do you know if your book keeping system is the right one for your business? It’s best to keep it as simple as possible for ...

Canadian QBO Conversion Issues | Problems That Aren't Really Problems

Why your balance sheet doesn't match QuickBooks Desktop after a QuickBooks Online-QBO conversion.

Can You Shred Scanned Receipts?

Learn CRA's and IRS's policies about accepting scanned receipts in place of original source documents ... they are different!

QuickBooks Online New User Interface | 2025 Canadian Rollout

Learn about the QuickBooks Online new user interface rolling out November 10th. Understand what's changing, how to prepare, and what it means for your books.

Organized Recordkeeping System - Home Based Office Filing System

What is the best recordkeeping system to get and stay organized so you can get rid of those drawers of stashed receipts? Simple choices and guidelines to eliminate stress and panic.

Paperless Security Guide

A step by step guide on how to keep your paperless documents safe and secure. The Paperless Security Guide is Brooks Duncan's third published guide.

Plooto Workflow | QBO Integration

Automate sending and receiving payments online with a Plooto workflow. Seamlessly integrates with QBO. Dual stage authorization.

LedgerSync Workflow | How It Works

LedgerSync workflow integrates with QBO and QBD. It automatically imports financial documents then pushes them to QuickBooks after coding and approval.

Profit First Method | Your Cash On Autopilot

The Profit First method is a system designed by Mike Michalowicz to help eradicate entrepreneurial poverty. Here's an overview and how to set it up in Canada.