- Home

- US Small Business Tax Compliance

- Form 1099-NEC

When to use the Form 1099-NEC

Independent Contractors - Non Employee Compensation Requirements

by L. Kenway BComm CPB Retired

This is the year you get all your ducks in a row!

Published June 8, 2024 | Updated November 14, 2025

WHAT'S IN THIS ARTICLE

What's New (OBBBA) | Difference between 1099-NEC vc 1099-K vs 1099-MISC | Form 1099 thresholds | Completing 1099 forms | Form 1099-NEC Highlights | Form 1099-K Highlights | Form 1099-MISC Highlights | How Commercial Contractor Registration and W-9 affect 1099 forms | FAQ About 1099 Reporting | Key Takeaways

What's New

OBBBA 1099-NEC, 1099-MISC, and 1099-K Threshold Changes

The One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025. It introduced changes to Form 1099s that U.S. small business owners need to understand and prepare for.

1099-NEC (Nonemployee Compensation) and 1099-MISC (Miscellaneous Income) increases in thresholds:

- 2025 payments maintains existing $600 threshold.

- 2026+ payments increases to a $2,000 threshold.

- 2027+ payments threshold is indexed annually for inflation.

- This change does not affect your W‑2 reporting for employees.

1099-K (Third-Party Network Transactions) threshold is $20,000 in aggregate payments AND more than 200 transactions in a calendar year effective for the 2024 tax year.

What has happened is that 1099-K lower thresholds approved in the American Rescue Plan Act (ARPA) are repealed. This returns the threshold to its previous level. Before the OBBBA was enacted in July 2025, the IRS had planned transitional thresholds for Form 1099-K to be: (1) 2024: More than $5,000 (no transaction limit); and (2) 2025: More than $2,500 (no transaction limit).

The OBBBA supersedes these planned ARPA changes, meaning the Act retroactively reinstated the $20,000/200+ transaction threshold for 2024 and all subsequent years.

IRS Form 1099-NEC vs 1099-MISC vs 1099-K: What's The Difference

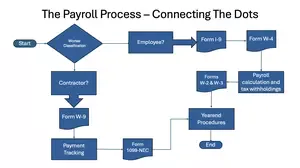

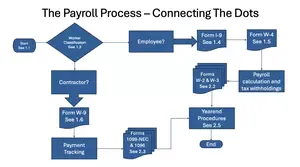

Generally a 1099 form is an IRS tax form that documents payments made a business, an individual, or an entity that is not an employee. Your task, as a small business owner, is to figure out the correct 1099 to file with the IRS by January 31st each year.

IRS introduced the form 1099-NEC Non Employee Compensation for the 2020 reporting of independent contractors compensation paid. Previously it had been reported in Box 7 of the Form 1099-MISC Miscellaneous Information. It can get confusing when you also consider the Form 1099-K Payment Card and Third-Party Network Transactions introduced in 2012.

Let's chat about the reporting requirements for non-employee compensation. If you are unsure whether someone is considered an employee or an independent contractor, please read my chat on the topic as it is a frequently audited area. A mistake in classification could be very costly to the employer.

OBBBA Form 1099 Thresholds Are Changing

1. IRS IR-2025-107 (October 23, 2025) retroactively reinstated the reporting threshold in effect prior to the passage of Implementation of The American Rescue Plan Act of 2021 (ARPA). This means TPSOs (third-party settlement organizations) are not required to file Forms 1099-K unless the gross amount of reportable payment transactions to a payee exceeds $20,000 and the number of transactions exceeds 200. This is retroactively in effect for the 2024 tax year.

Background History

2021 ARPA legislation was delayed two years in a row. The IRS issued Notice 2024-85 on November 26, 2024 providing guidance on transition relief for TPSOs. They are also known as payment apps and online marketplaces.

The 2024-85 notice provided that TPSOs would be required to report transactions on Form 1099-K when the gross amount of aggregate payments for those transactions, irrespective of the number of transactions, was more than $5,000 in calendar year 2024, $2,500 in calendar year 2025, and $600 in calendar year 2026 and after.

The 2025 OBBBA supersedes the planned ARPA changes.

2. With the passing of the OBBBA in July 2025, there are new thresholds. For Forms 1099‑NEC and 1099‑MISC, the general reporting threshold increases from $600 to $2,000 for payments made in 2026 and later years. Beginning with 2027 payments, the threshold will be indexed for inflation. For payments made in or before 2025, the $600 threshold still applies.

The separate reporting requirement for direct sales of consumer products totaling $5,000 or more (reported by checking a box on either Form 1099-NEC or Form 1099-MISC) remains unchanged by the OBBBA. [1]

Completing 1099 Forms

- When completing any IRS Form 1099, always use the individual's legal name for a sole proprietorship or independent contractor.

However, if the business operates under a DBA (doing business as), use the DBA name on the Form 1099.

When preparing the Form 1099 for a business or partnership, use the entity's name. - Even if you paid the Independent Contractor by credit card, PayPal or Venmo, you may still need to send a 1099-NEC for any amount paid by cash/cheque if the criteria (see below) is met.

Does this mean that some payments will not be captured on either the 1099-NEC, 1099-MISC or 1099-K? Yes but not your problem. Why? You don't know if the IC will receive a 1099-K. You don't know if the IC had over $20,000 in sales and over 200 transactions ('old' rules before 2024). - If you hire ICs, you want to be up on your independent contractor rules. A good place to start was the IRS webcast on 1099 MISC Filing requirements at www.irsvideos.gov. However, this portal has been shut down and the IRS now uses IRS YouTube to post its webinars. It's very unfortunate as they don't seem to be converting the old webinars to the new platform so a lot of good information is gone.

The transcript said it will cover "your responsibilities for filing Form 1099‑MISC and the corresponding Form W‑9. We will be discussing reporting of rents, nonemployee compensation, royalties, other income and gross proceeds to attorneys." Backup Withholding was also discussed including how to deposit it.

As the link to this webinar is no longer available, your best bet is the IRS website on Reporting Payments to Independent Contractors

Takeaway

As of 2020, non-employee compensation is no longer reported in box 7 of the Form 1099-MISC. It now gets reported on Form 1099-NEC. - Payments are reported on a calendar year not a fiscal year.

- Report any incorrect information on a 1099 form to the IRS as soon as possible.

Sources: IRS & AIPB & Tax Receipts.com

Form 1099-NEC Highlights

Why Does The IRS Require A Form 1099-NEC?

Under current law, only payments for services to any person engaged in business or trade that aggregated to $600 plus per year are reported. Until 2020 (2019 tax year), this income was reported on various 1099s including the 1099-MISC. The IRS reintroduced the 1099-NEC in 2021 for the 2020 tax year and it was successfully implemented.

For 2026, the OBBBA increases the threshold for Form 1099-NEC (and 1099-MISC) from the current $600 to $2,000.

One of the ways the IRS audits independent contractors is through the 1099 matching program. The IRS began matching Form 1099s to business returns to find underreported income. The matching was done after refunds had been issued. As refund fraud increased, the issue was addressed by the 2015 PATH (Protecting Americans from Tax Hikes) Act to fight against it.

In 2017, the IRS began scrutinizing income reported by matching it to 1099s filed before they issued a refund. This quick audit method is low hanging fruit and easy to audit thereby decreasing refund fraud while increasing its enforcement and assisting with the filing of more accurate tax returns. To allow for upfront matching, the IRS changed the required 1099s to be filed by January 31st instead of February 28th.

Letter CP2000 Notification of Underreported Income is sent if the information is mismatched. Find out why you received the notice and how to proceed before you reply.

Who Should Receive the 1099-NEC?

Here is a brief overview of 3 general rules about who should receive the 1099-NEC:

General Rule #1 Services Only:

Only required for services delivered, NOT product or materials, to your business are reported. This means (a) personal payments (such as birthday or holiday gifts, sharing the cost of a car ride or meal, or paying a family member or another for a household bill) and (b) wages to employees are not reported here.

General Rule #2 Payment Thresholds ($2,000 for 2026):

Only payments that total $2,000 or more ($600 for tax years prior to 2026) that were PAID DIRECTLY TO AN INDIVIDUAL are reported. An individual would be a sole proprietor, independent contractor, freelancer, a self-employed person, consultant, or a vendor.

In addition, any suppliers who do not file a corporate return are reportable. You need to ensure you have a W-9 on file to determine if an LLC requires a 1099-NEC or not because they have the option to file as a sole proprietor / partnership or as an S-Corp.

General Rule #3 Paid Through Bank:

Only payments made by cash or payments made through your bank account such as cheques, debits or direct bank transfer (ACH/debit) are reportable. Payments made by credit card or through payment apps like PayPal are reported by those processors on Form 1099-K (if thresholds are met).

Exception to the Rules:

Avalara*, experts in sales and use tax, explains that "Form 1099-NEC (or the 1099-MISC but not both) can also be used to “report sales totalling $5,000 or more of consumer products to a person on a buy-sell, a deposit-commission, or other commission basis for resale.”

General Rule*:

Issue Form 1099-NEC to all law firms, regardless of their tax filing status

*Source: House approves new thresholds for 1099 forms by Gail Cole; 1099 Rules for Attorneys and Law Firms by LawPay

Who Should Not Receive the 1099-NEC?

- Payments to corporations are not reported on the 1099-NEC; this includes LLC, S Corps, and C Corps.

- Wages paid to employees

- Employee business travel allowances paid under an non-accountable plan (this goes on W-2 and is subject to applicable federal employment taxes)

- Expense reimbursement under an accountable plan are not taxable or reportable

- Freight, storage, or merchandise payments

- Real estate agents are not considered individuals for these purposes so do NOT report rent paid to real estate agents.

- Commercial Contractor Registration or W-9 (captures TIN (taxpayer identification number), etc. when a person or entity is required to report certain types of income)

- Payments made through a third party provider such PayPal, Venmo, or a credit card provider will be captured on Form 1099-K by the third party. They are not your responsibility. You do not issue a 1099-NEC for any payments made through these channels, even if they are under the 1099-K thresholds.

1099-NEC Yearend Tax Compliance Reminder

for Independent Contractors

- As of the 2020 tax year, you now use Form 1099-NEC to report independent contractor payments instead of the Form 1099-MISC (box 7) as in prior years.

- Form 1099-NEC should be presented to service contractors before February 1, 2021. IRS receives Copy A, the contractor receives Copy B, and you retain Copy C for your records to support your subcontractor expenses.

- You may file the forms using a truncated taxpayer identification numbers (TTIN) ... the first five digits are replaced with an "x" or "*" ... to prevent identity theft.

- The IRS receives Form 1096 Annual Summary and Transmittal of U.S. Information Returns AND Copy A by March 1 ... March 31 if filed electronically.

- To send the 1099s by email requires the explicit permission of the contractor.

- Annual Return Form 945 Withheld FIT is used to report non payroll payments including WFIT on Form 1099 is also due January 31, 2021.

As Robert Wood, tax lawyer and Forbes columnist likes to say, "It's better to give than receive." :)

Source: The Bookkeeper's Notes Newsletter

Key Takeaway Form 1099-NEC

✅ Do This

- Ensure you file a 1099‑NEC when total payments to a nonemployee reach (1) $600 for payments made through 2025, and (2) $2,000 for payments made in 2026 and later (indexed 2027+).

- Remember the January 31st deadline is for both the IRS and the recipient.

- Electronically file if distributing 250 or more forms.

- Ensure you have a W-9 on file. A W-9 (captures TIN (taxpayer identification number), etc. when a person or entity is required to report certain types of income.

❌ Not This!

- Don’t use Form 1099-MISC for non-employee compensation after 2019.

Form 1099-K Highlights

How The IRS Knows You Didn't Report Income

The IRS has many ways to determine if they suspect you have unreported income. Here are a few:

- Information statement matching where forms 1099, W-2, etc are matched to your personal income tax returns filed with IRS.

- Comparing your business financial ratios with similar businesses. (Check out BizStats to see how your business compares.)

- Website e-commerce activity are matched to 1099-K forms are matched to your business income reported and filed with the IRS.

- Bank deposit analysis where they look at all the monies deposited to you and your family members' bank accounts.

- Lifestyle audits, also sometimes referred to as T-account analysis, where they compare reported income to personal expenditures. It's not good for you if they resort to this type of audit.

In 2012, they targeted unreported online income by introducing the Form 1099-K Payment Card and Third-Party Network Transactions. The legislation for this was enacted in 2008. Processors of credit card and debit cards such as Visa and Master Card as well as electronic payment systems like PayPal and Venmo are required to report the gross receipts of payments made to businesses. This reporting did not affect cash receipts.

As mentioned earlier, this is a quick audit method that catches low hanging fruit. It is easy to audit which decreases refund fraud and increases its enforcement. This matching program assists with the filing of more accurate tax returns.

What Is The Form 1099-K and Who Should Receive?

Prior to 2025, the form 1099-K Payment Card and Third Party Network Transactions details payments received through payment card transactions and third-party network transactions was issued if you met or exceeded both 200 transactions and $20,000 in gross total reportable payment volume.

On November 26, 2024, the IRS issued transition guidance for new thresholds for the form 1099-K. They are: $5,000 in 2024, $2,500 in 2025, and $600 in 2026 and thereafter irrespective of the number of transactions. This means if you receive payment card transactions or third-party network transactions totalling to the new thresholds or more in a calendar year, you'll receive a Form 1099-K.

It’s generally filed by third-party payment processors like PayPal, Stripe, or Square. If you’re a business owner that has receives online payments, you’ll receive a 1099-K form each year, summarizing your transaction details if you exceed the stated thresholds.

This change was designed to improve tax compliance and ensure that income received through such TPSO platforms are reported accurately to the IRS. As a small business owner, you should prepare for these reporting requirements, as they may impact how you track and report income. Additionally, it's extremely important to keep accurate records of all your transactions to ensure you are reporting your income correctly.

Takeaway

Filing is typically handled by the payment processing service. As a merchant, ensure your business information is up-to-date in these services to receive accurate and timely forms.

If you haven't already done so, it might be a good idea to reach out to your accountant or a tax professional to make sure you're clear on what to expect and how to handle any issues that might arise from these new thresholds for the 1099-K.

What To Do If You Receive A 1099-K?

If you receive a 1099-K, ensure these amounts are included in your income to the IRS.

Key Takeaway Form 1099-K

✅ Do This

- Check personal business information for accuracy on these platforms.

- Verify the sum of the payments against your own records to prevent discrepancies that might trigger an audit.

- Keep detailed records of all transactions, including invoices, contracts, and communication, to support your filings and clarify any discrepancies during an IRS audit.

❌ Not This!

- Don’t ignore errors in transaction reports; they can lead to misfiled taxes and possibly trigger an audit.

- Third party processors are essential for businesses processing a significant volume of payments through online activity. Don't stop using them just because you might receive a form 1099-K.

Form 1099-MISC Highlights

What Is The Form 1099-MISC and Who Should Receive?

The form 1099-MISC Miscellaneous Income used to be used for reporting of independent contractors compensation paid. Since 2020, these payments are now reported on Form 1099-NEC. This reporting change did not make the 1099-MISC go away. It is still used for various forms of alternative income like rents, prizes, awards, healthcare payments, and other payments not involved with non-employee compensation.

You need to file Form 1099-MISC for each person from whom you have withheld any federal income tax under the backup withholding rules regardless of the amount, or for whom you have paid at least $10 in royalties or $600 in rents, services (other than nonemployee compensation), prizes, awards, or other income payments.

Filing can be filed by paper or electronically. Check whether your specific payer software supports electronic submissions to simplify the process.

What To Do If You Receive a 1099-MISC?

As with the other 1099 forms, if you receive a 1099-MISC, ensure these amounts are included on the appropriate line when filing your income tax return with the IRS.

Key Takeaway Form 1099-MISC

✅ Do This

- File a Form 1099-MISC for each instance of miscellaneous income over $600.

- Pay attention to different deadlines depending on the type of payment.

- Keep detailed records of all transactions, including invoices, contracts, and communication, to support your filings and clarify any discrepancies during an IRS audit.

❌ Not This!

- Don’t confuse it with 1099-NEC which is now used for reporting non-employee compensation.

Commercial Contractor Registration and W-9s

What is a W-9?

This form is used by businesses to gather information from contractors, freelancers, or vendors from whom they will need to report payments for federal tax purposes.

When a business entity hires these non-employees, they are required to fill out a W-9, which provides the business with necessary details such as the contractor's name, address, and Taxpayer Identification Number (TIN), which is typically a Social Security Number (SSN) or Employer Identification Number (EIN).

More >> Form W-9 and Form 1099-NEC

For individuals, such as freelancers or contractors, who complete a W-9, the information provided is used by the business to file a 1099 form. For example, Form 1099-NEC is used to report payments of $600 or more in the course of the year to a non-employee.

Their completion of the W-9 should provide documentation to prove if the entity is exempt from a 1099-NEC filing.

In practice, both a W-9 and a 1099-NEC are usually necessary for the reporting process but serve different roles. The W-9 is used to collect the needed identification data, which is subsequently used to fill out and submit a 1099-NEC when it comes time to report payments made.

What is Commercial Contractor Registration?

This term usually refers to a required registration process for contractors who work for commercial entities, often regulated at the state level.

The specific rules and requirements vary depending on the state. Typically, this involves registering with a state contractor's board or similar regulatory body, often necessary for legal operation and bidding on contracts.

The Commercial Contractor Registration in itself doesn't directly interact with IRS forms like W-9 and 1099. However, maintaining proper registration and compliance affects a contractor’s business operations, including their eligibility to receive payments, which in turn, require reporting through IRS forms.

Contractors must be registered (where necessary) and compliant to facilitate their tax obligations, such as those involving the submission of Form 1099s by their clients based on the information provided in W-9 forms. Their registration should show if the entity is exempt from a 1099-NEC filing.

Key Takeaway

✅ Do This

- Require a contractor to fill out a W-9 when beginning a relationship with a your business.

- Ensure the W-9 information is correct as your business uses this information to properly fill out a form 1099-NEC form when reporting to the IRS.

- If you can't reach a vendor to get their W-9 information, it is recommended you make several attempts using the same email thread or log your calls or text messages. Save these as proof your business did its due diligence in attempting to issue a form 1099-NEC.

- The Commercial Contractor Registration, on the other hand, is more about the licensure and legal status of the contractor which indirectly impacts tax and payment processes managed through forms like W-9 and 1099-NEC.

- Use the Central Contractor Registry (I believe it's also called IRS TIN Matching) for TIN matching. Make this part of your onboarding process. DUNS number is public information, EIN is not. TIN matching reduces IRS fines and saves you admin time. I found a 2010 guide to the system here. It's an old version but maybe it can help you find a more current version.

❌ Not This!

- Don't pay a vendor if they have not provided you with a completed W-9.

FAQ About 1099 Reporting

These Q&A are a direct excerpt from the "Common Questions" section of an IRS 2011 webinar on Form 1099 Reporting for Federal Agencies. I believe the responses provided are still valid in 2024.

What if a vendor provides service part of the year under one TIN then provides the remainder under another?

What if a vendor provides service part of the year under one TIN then provides the remainder under another?

Depends on W-9 entity information

- If sole proprietor gave SSN & now gives EIN without change of entity type, use SSN, put individual’s name on 1st line of 1099 and business name on 2nd line.

- If changing from sole proprietor to corporation or if company has changed hands, issue separate 1099s.

What if a vendor is exempt and I inadvertently sent a 1099?

What if a vendor is exempt and I inadvertently sent a 1099?

Prepare a new 1099

- Enter “X” in the “CORRECTED” box

- Enter payer, recipient, and account no. exactly as it appeared on the original incorrect 1099

- Enter zero money amount in correct box

Where do I send the information returns?

Where do I send the information returns?

Internal Revenue Service Center listed for your area on the Form 1096 Instructions (250 or more magnetic media).

Can I file an extension to file Forms 1099?

Can I file an extension to file Forms 1099?

Yes! Send Form 8809 to the address shown by Jan. 31 for a 30 day extension.

What if I can’t get a Form W-9 or the Form W-9 information from the recipient?

What if I can’t get a Form W-9 or the Form W-9 information from the recipient?

Backup withholding applies. Backup withholding is income tax withholding at the source for non-payroll types of payments and compensation. In 2024, it 24%. It begins immediately if

- Payee was paid more than $600 in prior year and an information return was issued, or

- Payee was subject to backup withholding in the prior year.

Backup withholding is reported on 1099-NEC box 4 and/or box 5. Form 945 is used to report and pay backup withholding to the IRS. These should be separate from form 941 deposits.

How long do I keep copies of information returns?

How long do I keep copies of information returns?

Three years from the due date, unless backup withholding applies (4 years).

Can I use photocopies of Forms 1099?

Can I use photocopies of Forms 1099?

No. You can get official forms at IRS offices or by calling 1-800-TAX FORM

How about substitute Forms 1099?

How about substitute Forms 1099?

Yes, if they meet the requirements of Publication 1179

Key Takeaways

- Since 2020, Form 1099-NEC Non Employee Compensation is for the reporting of independent contractors compensation paid over $600 in a calendar year.

- Since 2012, Form 1099-K Payment Card and Third-Party Network Transactions details payments received through payment card transactions and third-party network. In 2024, thresholds changed to transactions that meet or exceed $5,000 in 2024, $2,500 in 2025, and $600 in 2026 and after in gross total reportable payment volume, irrespective of the number of transactions.

- The Form 1099-MISC Miscellaneous Income is still used for various forms of alternative income like rents, prizes, awards, healthcare payments, and other payments not involved with non-employee compensation.

- Thresholds for all three forms are expected to change in 2024 or 2025.

- The Form W-9 and the Commercial Contractor Registration are usually necessary for the reporting process. The information collected (and verified) is used to complete your 1099 forms.

- The deadline for 1099 forms is January 31st. Payments are reported on a calendar year basis.

Tracing History - Form 1099 Thresholds

The following historical information describes proposed changes that were superseded by the OBBBA before implementation. It is included here for context only.

June 2024

Form 1099 Thresholds Are Changing

1. Implementation of The American Rescue Plan Act of 2021 legislation was delayed two years in a row. The IRS issued Notice 2024-85 on November 26, 2024 providing guidance on transition relief for TPSOs (third-party settlement organizations). They are also known as payment apps and online marketplaces.

The notice provides that TPSOs will be required to report transactions on Form 1099-K when the gross amount of aggregate payments for those transactions, irrespective of the number of transactions, is more than:

- $5,000 in calendar year 2024

- $2,500 in calendar year 2025

- $600 in calendar year 2026 and after

The multi-year delay and phased implementation in Notice 2024-85 were intended to address the substantial administrative and compliance burdens the sudden $600 threshold would place on both TPSOs and casual sellers, many of whom might not have realized their small-scale transactions would become reportable. The extended timeline allowed the IRS to provide more comprehensive guidance and gave all affected parties more time to update their systems and understand their tax obligations.

2. H.R. (House of Representatives) 7024 Tax Relief for American Families and Workers Act of 2024 passed in January 2024 and has now gone to the Senate. On August 1, 2024, the broad tax bill finally reached the Senate floor, but a vote to end debate failed, 48-44, largely on party lines. It did not pass and never became law. If passed into law, the thresholds would have been:

- 1099-MISC and 1099-NEC will change from $600 to $1,000 for payments made in 2024. Future years would be tied to inflation.

- Direct sales threshold would change form $5,000 to $1,000.

However, the provisions of H.R. 7024 regarding 1099 form thresholds were later incorporated into a different piece of legislation, which was enacted into law as the "One Big Beautiful Bill Act" (OBBBA) on July 4, 2025. The direct sales thresholds were not changed in the OBBBA and remain at $5,000.

[1] H.R. (House of Representatives) 7024 Tax Relief for American Families and Workers Act of 2024 passed in January 2024 and has now gone to the Senate. On August 1, 2024, the broad tax bill finally reached the Senate floor, but a vote to end debate failed, 48-44, largely on party lines. It is doubtful it will pass before the November elections. It proposed the following thresholds: (1) 1099-MISC and 1099-NEC will change from $600 to $1,000 for payments made in 2024. Future years would be tied to inflation. (2) Direct sales threshold would change from $5,000 to $1,000.

My sincere gratitude to all my readers ... without you I'd have no website. Blessings to you all. My suggestion to you ... enjoy a tall cool glass of lemon water while you click and poke and peek and snoop this site ... perhaps start with the blog which lists the most recent updated articles.

I Hope You Enjoy Your Visit Today,

Your Tutor

You might like these

U.S. Employment Tax Forms | Yearend Guide For Small Business Owners

U.S. employment tax forms W2, W3, W4, I-9 and year-end payroll tasks. A small business owner's guide to closing out the year right.

U.S. Self-Employment Income | Self-Employment Tax

Self-employment income is subject to U.S. self-employment tax. You'll find information on estimated taxes, standard mileage rates and U.S. rules for business use of your car.